Skip to content

Home

Research

Papers

Coding

Articles

Audio Papers

Software

News Sentiment Analysis Tool

Factor Tracker

R-Candles

Trading

Contact Us

Home

Research

Papers

Coding

Articles

Audio Papers

Software

News Sentiment Analysis Tool

Factor Tracker

R-Candles

Trading

Contact Us

Coding

How to Get Free Full Crypto Intraday Data (2013–2025) From Kraken

Daily + 15:45 OHLCV: A Database for Reliable Backtesting

Historical Constituents of an Equity Index in Python (Norgate Data)

Building a Survivorship Bias-Free Crypto Dataset with CoinMarketCap API

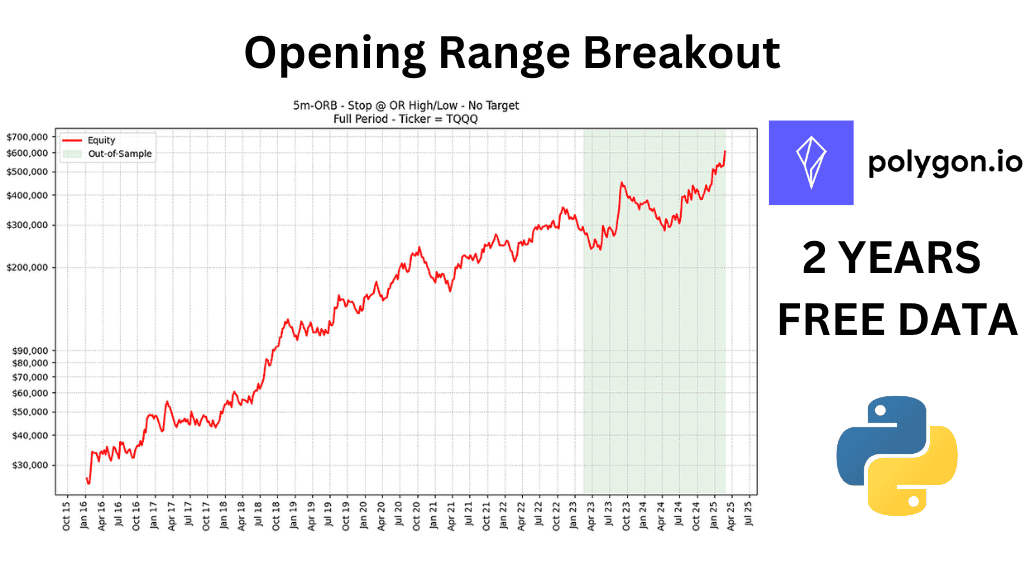

Backtesting the Opening Range Breakout (ORB) Strategy in Python using Polygon.io

How to Construct a Survivorship bias-free Database in Norgate using Python

Backtest a Profitable Trend-Following Strategy using Python

Backtest a Profitable Trend-Following Strategy

Designing a Profitable Intraday Strategy Using Python and Alpaca

Backtesting 2 Years of FREE Data Using Python: Enhancing SPY Momentum Strategies with Polygon, from ‘Beat the Market’

MATLAB: Backtesting “Beat the Market: An Effective Intraday Momentum Strategy for the S&P500 ETF (SPY)”

CONCRETUM | GROUP

×

Home

Research

Papers

Coding

Articles

Audio Papers

Software

News Sentiment Analysis Tool

Factor Tracker

R-Candles

Trading

Contact Us